Only you know what you want your retirement to look like. If your practice is incorporated and you are looking for a more significant nest egg with even better income tax protection than a Registered Retirement Savings Plan (RRSP), an Individual Pension Plan (IPP) could be the answer.

What is an IPP and how does it work?

An Individual Pension Plan is a defined-benefit pension plan that is typically set up for just one plan member and is designed for dental professionals like you.

With a similar income structure to an RRSP, an IPP has better tax protection and a much higher corporate contribution limit. Tax-deductible contributions are made directly from your corporation to the IPP. The assets of the IPP are invested and grow tax-sheltered. When you retire, the IPP provides you with a lifetime monthly pension or you can further defer taxes by making a lump sum transfer of the value of the IPP to an RRSP or LRIF/RRIF1.

What are the requirements of an IPP?

• Your business is required to be incorporated (professional, regular, personal services corporation)

• Some or all of your income from your corporation must be paid to you as T4 employment income

Should incorporated dentists consider an IPP?

An IPP can create a significant tax-planning opportunity for you and your business because the corporation can make tax-deductible contributions and you can benefit from tax-deferred growth inside the plan. Both of these benefits help with the Canada Revenue Agency’s (CRA) rules on passive investment income: the tax deduction helps reduce the corporation’s active income, and the taxdeferred growth lowers corporate investment income.

In Quebec, Ontario, Manitoba, Alberta and British Columbia, IPPs now offer enhanced flexibility with no locked-in requirement and fully flexible funding that is responsive to your cashflow needs.

This enhanced flexibility is a significant improvement for incorporated professionals who currently have or would like to setup an IPP.

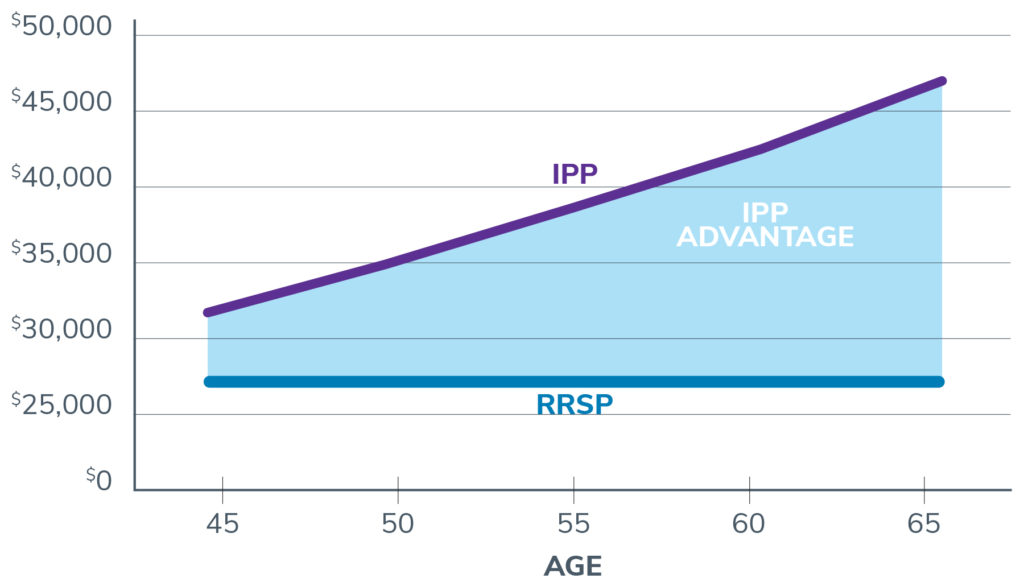

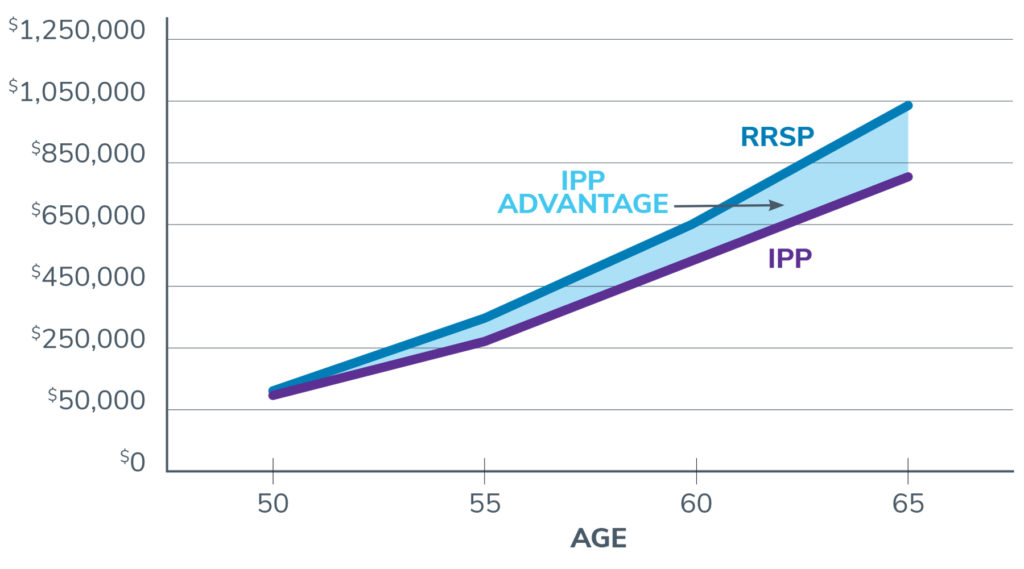

Higher Tax-deductible Contributions

• Higher Annual Contributions – the IPP increases from 18% at age 39 to 29% at age 65 whereas an RRSP is 18% for all ages

• Over the years, the IPP offers your corporation 100’s of thousands of additional tax deductible contributions as compared to a personal RRSP

• Flexibility in making contributions to IPPs

[table id=26 /]

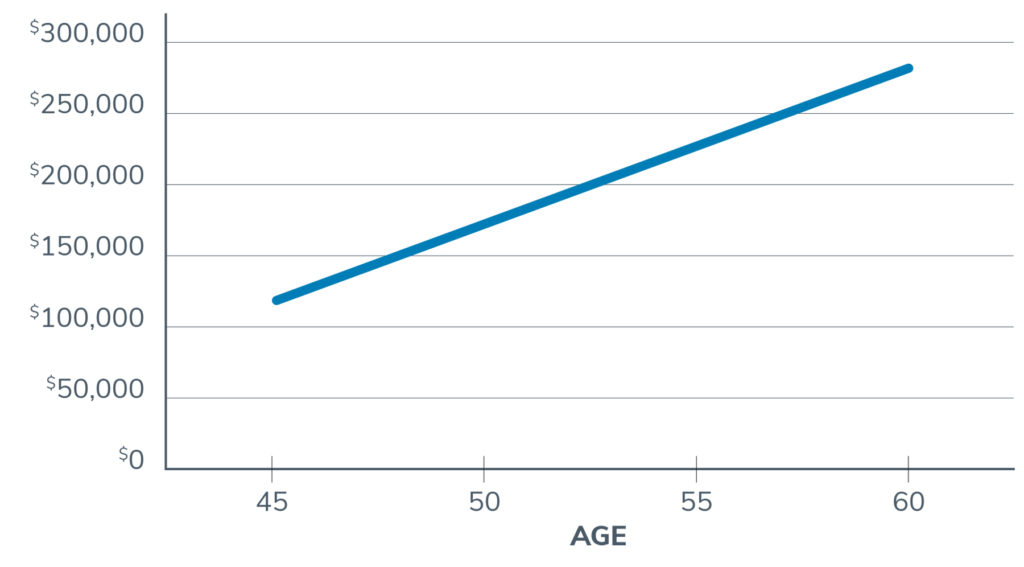

Contributions — Past Service2

Tax-deductible Corporate Contributions

• Flexibility to make contributions – immediately or amortised over a number of years

• Higher if the plan member has unused RRSP contribution room

• Increases with age and past service

[table id=27 /]

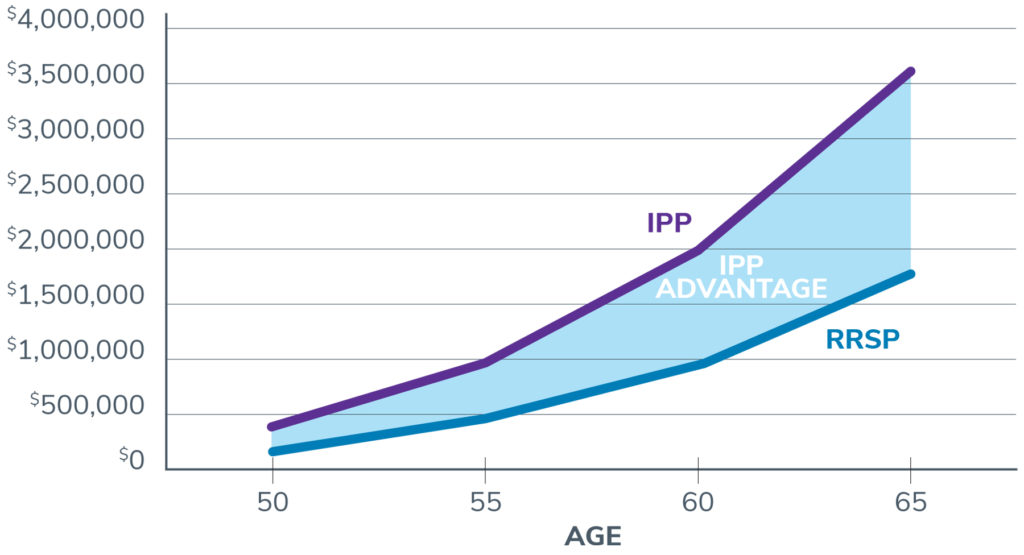

Tax-sheltered Savings2

• Significantly higher tax-sheltered savings relative to an RRSP

• Tax savings & growth of these savings over time

• Ability to save more and the growth of these contributions tax sheltered

• Intergenerational wealth transfer strategies available for family IPP’s where children of owners are earning T4 income from the corporation

[table id=28 /]

Terminal Funding2

Retiring early (prior to 65)

• additional tax-deductible contributions

Additional IPP benefits of retiring early

• Bridge Pension (CPP/OAS) to 65

• Decreased reduction for earlier start of pension

[table id=29 /]

Corporate Taxes & Impact on Passive Income Rules2

• Reduces impact of Passive Income Rules – At worst, delays, and at best, eliminates the impact of the passive income rules on eligible corporations

• Assumes the corporation elected to make the full past-service contribution at first opportunity

• In addition to the higher retirement savings, estimated corporate tax savings of over $200,000

[table id=30 /]

If you have questions about planning for your retirement, an Individual Pension Plan might be the answer.

• Lowers Corporate Taxes

• Higher Tax-Deductible Contributions

• Higher Tax-Sheltered Retirement Savings

• Additional Contributions for Service

• Tax-sheltered Wealth Transfer

• Creditor Protection

• Passive Income Rule (Reduces/ Eliminates)

• Funding Shortfall

• Plan Expenses are Tax Deductible

Why CDSPI?

CDSPI’s investment solutions are built solely with the needs of Canadian dental professionals in mind. Our Investment Planning Advisors3 are CERTIFIED FINANCIAL PLANNER® (CFP®) professionals who take the time to understand your unique needs and always provide objective, unbiased advice—because they never receive third-party commissions from the investments they recommend.

Our advisors can help you to understand the different options available that give you the flexibility to adapt to changes in your financial situation over the course of your career. Our goal is to support your financial plan for today and into the future.

At CDSPI we take the time to get to know who you are, where you are in your life and career and where you want to be. This includes a commitment to:

• Develop an understanding of your retirement goals and objectives

• Review your current financial situation

• Present you with a thorough analysis and recommendations that are in your best interests

• Implement a strategy and commit to regular review

• Listen to your feedback

• Stay in touch and informed about your business and your plans

If you would like additional information about how an Individual Pension Plan can support your retirement plans, please contact CDSPI.

1. A Portion may have to be paid in cash (taxable) on windup

2. Contributions are tax-deductible to the corporation; All amounts are estimates only and based on the following:

a. Maximum funding rules applicable for funding of designated pension plans based on tax rules in 2021 (ITR 8515)

b. T4 Earnings in each year that produces maximum IPP benefit, i.e., $162,278 in 2021

c. Setup at age 45 with 15 years of past service and no RRSP contribution room, funding flexibility allows funding to be immediate or spread over a number of years

d. Canadian Controlled Private Corporation (CCPC) eligible for Small Business (SMB) Tax Credit; Corporate Income of $350,000 & Retained Earnings of $300,000.

3. Advisory services are provided by licensed advisors at CDSPI Advisory Services Inc. Restrictions may apply to advisory services in certain jurisdictions.

The content of this page is intended for information purposes only and to facilitate discussion only. All amounts are estimates only and are based on the assumptions made.

This information is not intended to offer taxation, legal, accounting or similar professional advice, nor is it intended to replace the advice of independent tax, accounting or legal professionals. Any tax-related information is applicable to Canadian residents only and is in accordance with current Canadian tax law.